Wednesday June 24, 2026 2:37 pm ECONOMYNEXT – In a notable policy reversal, Sri Lanka’s National People’s Power (NPP) government, led by President Anura Kumara Dissanayake, decided not to implement a key Value Added Tax (VAT) reform announced in the 2026 Budget. The proposal to…

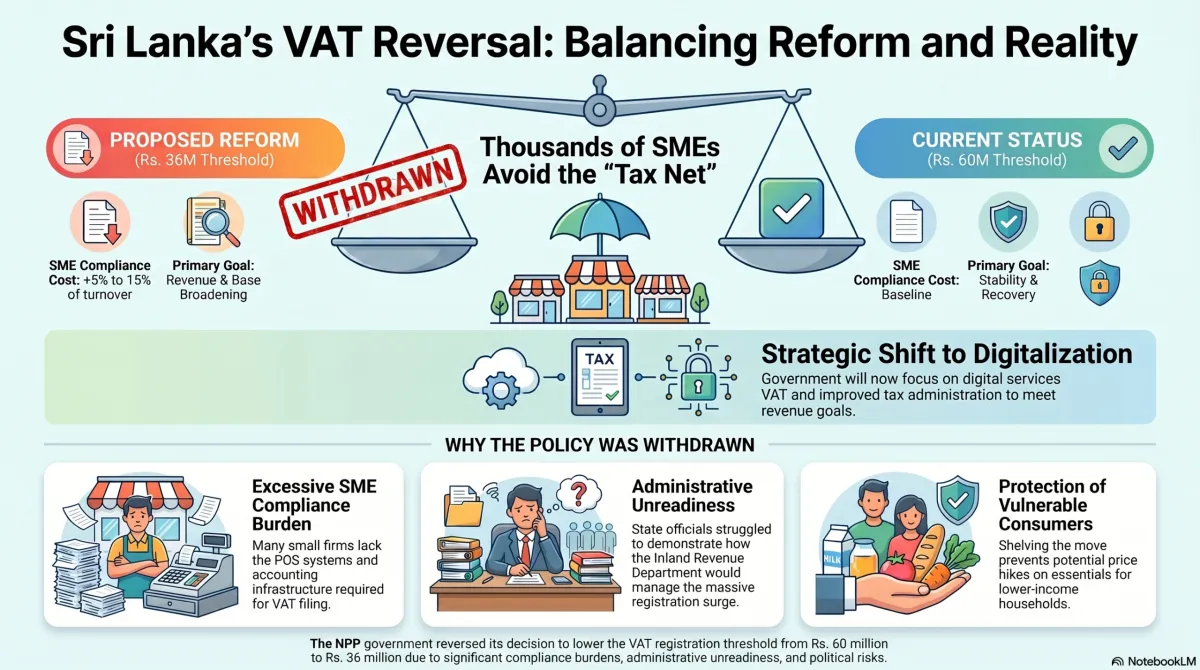

Wednesday June 24, 2026 2:37 pm ECONOMYNEXT – In a notable policy reversal, Sri Lanka’s National People’s Power (NPP) government, led by President Anura Kumara Dissanayake, decided not to implement a key Value Added Tax (VAT) reform announced in the 2026 Budget. The proposal to lower the VAT registration threshold through the amendment from Rs. 60 million to Rs. 36 million annual turnover effective from July 1 has been dropped. The decision, announced in Parliament on Tuesday (23), reflects the tension between fiscal reform goals and political realities in a post-crisis economy. The NPP government’s decision to abandon the VAT threshold reduction illustrates the complex interplay between economic reform, political reality, and social impact in Sri Lanka. While broadening the tax base remains essential for long-term fiscal stability, the government has prioritized protecting vulnerable businesses in the short term. The amendment, included in the VAT (Amendment) Bill gazetted in late April 2026, sought to broaden the tax base by requiring more businesses to register for VAT and the Social Security Contribution Levy (SSCL). The Parliament Committee on Public Finance (COPF) last week exposed the unpreparedness of the government as state officials struggled to respond to questions raised by the panel members. Previously, businesses with annual turnover exceeding Rs. 60 million were required to register. The new threshold would have brought thousands of medium and small enterprises with turnover between Rs 36 million into the formal tax net. The stated goal was to increase tax revenue, reduce distortions between registered and unregistered businesses, and support fiscal consolidation. The move aligned with broader 2026 Budget measures, including VAT on digital services by non-residents and adjustments to financial services taxation. ✓ WhatsApp Channel Follow EconomyNext for live updates Breaking news · Instant alerts · Exclusives Follow Now Impacts on SME, Consumers The change would have imposed significant compliance burdens on the small and medium sector businesses. Newly registered businesses would need to maintain detailed records, issue VAT invoices, use point-of-sale (POS) machines, file regular returns, and remit taxes. Many SMEs lack sophisticated accounting systems, potentially increasing administrative costs by 5–15 percent of turnover for smaller players. Critics argued it could force artificial business splitting or push firms toward the informal economy. Registered businesses can claim input tax credits, but the initial adjustment often leads to price increases as costs are passed on. Lower-income consumers reliant on small retailers could face higher prices for essentials, potentially contributing to inflationary pressure in an already fragile economy. Overall, the move was projected to generate additional revenue of several billion rupees but at the risk of slowing SME recovery and employment in a sector that employs the majority of Sri Lankans. Practical Difficulties Implementing the lower threshold presented several challenges. Many SMEs in retail, services, and small manufacturing lack the infrastructure for VAT compliance. The Inland Revenue Department (IRD) would face a massive increase in registrations, straining its resources for audits and support. Moreover, SMEs are still recovering from high inflation, supply chain issues, and reduced consumer demand after the 2022 economic crisis. Adding regulatory burden could lead to business closures or reduced investment along with administrative and transitional issues as effective rollout would require extensive training, updated IT systems, and a grace period, which appeared rushed in the original timeline. There was also a risk of tax evasion. Businesses near the threshold might under-report turnover, leading to enforcement challenges and potential corruption. These practical hurdles made the policy contentious even among tax experts who supported base-broadening in principle. Political Implications The decision to drop the proposal is a pragmatic retreat for the NPP government, which came to power on an anti-establishment, pro-people platform. SMEs and small traders form a significant voting base in Sri Lanka. Implementing the change risked alienating this group ahead of future elections, especially given the government’s promises to ease the cost-of-living burden. There was a strong opposition from business chambers, trade unions, and opposition parties framed the move as anti-SME. Shelving it helps the government project responsiveness and sensitivity to ground realities. Though the move avoids short-term pain, repeated policy reversals could undermine the government’s reformist image and signal weakness in fiscal discipline. This U-turn highlights the classic dilemma faced by reformist governments in Sri Lanka: balancing long-term fiscal health with short-term political survival. IMF Proposal? Sri Lanka’s ongoing Extended Fund Facility (EFF) program emphasizes revenue mobilization and tax base broadening to achieve primary surplus targets and debt sustainability. Lowering the VAT threshold aligns with standard IMF advice on expanding the tax net and reducing exemptions. However, the IMF typically allows flexibility on implementation timelines when domestic pushback is strong, provided overall fiscal targets are met through alternative measures like better enforcement or other revenue streams. The NPP government’s decision to drop this specific measure does not appear to have derailed broader program negotiations, suggesting it was a domestically driven adjustment rather than an IMF-mandated one. Representations from SME associations, chambers of commerce, and opposition highlighted potential job losses and economic slowdown if the VAT was imposed on small businesses. With the economy still fragile and cost-of-living concerns high after the fuel price hikes, imposing new burdens in mid-2026 was politically risky. The government likely assessed that pushing the bill could invite prolonged debate, amendments, or even internal divisions within the NPP alliance. The government appears confident in meeting fiscal goals through improved tax administration, digitalization, and other measures such as digital services VAT, making the controversial threshold cut less urgent. The government’s decision underscores a broader truth: successful tax reform in Sri Lanka requires not just sound policy design but also careful sequencing, stakeholder consultation, and robust administrative readiness. As the country navigates its IMF program and post-crisis recovery, future attempts at base-broadening will likely need stronger mitigation measures such as simplified compliance for small businesses or phased implementation to gain public and political acceptance. (Colombo/June 24/2026)